Oftentimes when clients approach me, they have heard about the different types of bankruptcy but aren't sure which one is right for them. The two common types of bankruptcy that individuals files are Chapter 13 and Chapter 7. In this post we'll discuss the difference between Chapter 13 and Chapter 7 bankruptcy.

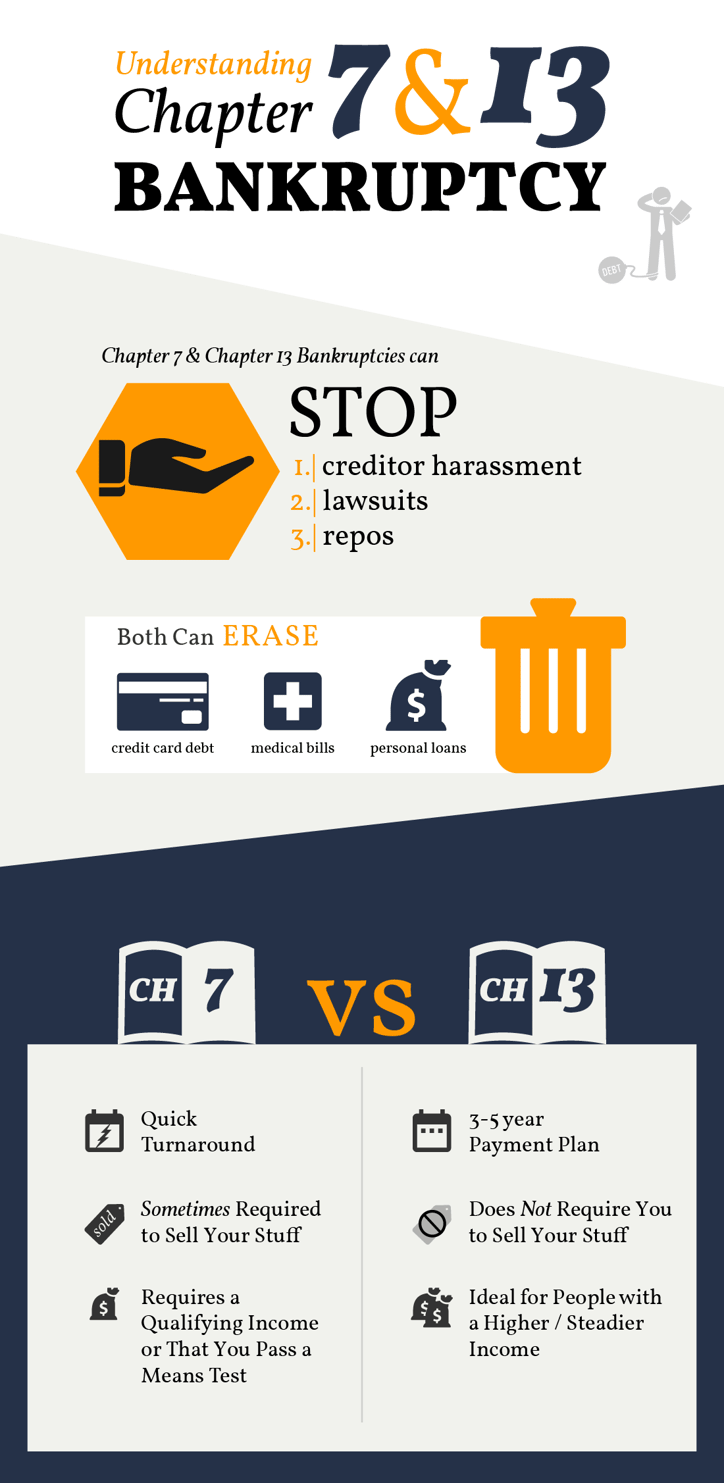

Chapter 7 is a liquidation bankruptcy designed to wipe out your general unsecured debts such as credit cards and medical bills. To qualify for Chapter 7 bankruptcy, you must have little or no disposable income. If you make too much money, you may be required to file a Chapter 13 bankruptcy (discussed below).

See below for a Chapter 7 vs Chapter 13 comparison chart.

Chapter 7

When you file for Chapter 7 bankruptcy, a trustee is appointed to administer your case. In addition to reviewing your bankruptcy papers and supporting documents, the Chapter 7 trustee’s job is to sell your nonexempt property to pay back your creditors. If you don’t have any nonexempt assets, your creditors receive nothing. As a result, Chapter 7 bankruptcy is typically for low income debtors with little or no assets who want to get rid of their unsecured debts.

Chapter 13

Chapter 13 is a reorganization bankruptcy designed for debtors with regular income who can pay back at least a portion of their debts through a repayment plan. If you make too much money to qualify for Chapter 7 bankruptcy, you may have no choice but to file a Chapter 13 case. However, many debtors choose to file for Chapter 13 bankruptcy because it offers many benefits that Chapter 7 bankruptcy does not (such as the ability to catch up on missed mortgage payments)

In Chapter 13 bankruptcy, you get to keep all of your property (including nonexempt assets). In exchange, you pay back all or a portion of your debts through a repayment plan (the amount you must pay back depends on your income, expenses, and types of debt). For this reason, Chapter 13 is commonly referred to as a reorganization bankruptcy. Typically, Chapter 13 bankruptcy is for debtors who can afford to make monthly payments to get caught up on missed mortgage or car payments or pay off nondischargeable debts such as alimony or child support arrears.

Next Steps

If you are considering bankruptcy and would like to explore all of your options, we offer a free consultation with one of our experienced lawyers. Please call  , or schedule an appointment by clicking the button below.

, or schedule an appointment by clicking the button below.

Comparison Chart